College education

If you start the planning process early enough, then affording a college education for your little ones isn’t too out of reach. Here at PlanKidsFuture, we have put together a quick guide for you on how best to fund your child’s, or grandchild’s college education.

Now, it is common knowledge that total cost of college has been slowly increasing over the past ten years, more so than the rate of inflation. In fact, there are indications that the yearly increases in costs are levelling out somewhat. Looking at 2013-2014 the increases in school fees were around 3.5% across the board.

Now, it is common knowledge that total cost of college has been slowly increasing over the past ten years, more so than the rate of inflation. In fact, there are indications that the yearly increases in costs are levelling out somewhat. Looking at 2013-2014 the increases in school fees were around 3.5% across the board.

Understandably, finding the money to pay for college isn’t a simple task for a lot of people. It is a similar financial commitment in terms of value, to buying a new car each year. However, by planning ahead, the impact can be significantly reduced. Take a look at the points made below for some useful pointers about saving for a college fund.

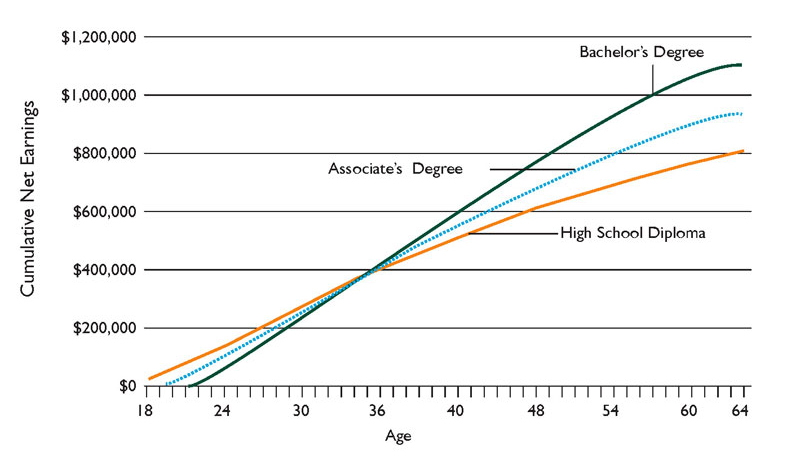

Estimated Cumulative Full-Time Earnings (in 2011 Dollars) Net of Load Repayment for Tuition and Fees, by Education Level

-

Don’t Delay

Any value of contribution or savings will soon add up if they are given enough time to mature. Starting at a lowly figure of just $50-$100 per month for a long period of let’s say 16-18 years will slowly develop into a nice nest egg for when the time comes.

-

Consider Your Own Retirement

There will be more places for your children to get access to college money after you have stopped working. So, it’s important to make sure that you give careful thought and consideration as to when you are going to retire, before putting money away for a college fund.

-

Benefit from a 529 or Coverdell Savings Arrangement

Did you know that certain, pre-qualified withdrawals can be made without federal taxes? Regardless of your income, you can open a 529 savings plan. There are no limits on the age of the beneficiary either so these are popular plans for grandparents and parents alike as you can deposit quite significant amounts. In some cases, this is in excess of $250k for each beneficiary. With a Coverdell savings account, you get almost the same tax advantages as the plan mentioned above. However, your contributions are capped at roughly $2k per year. They are also really straightforward to manage.

-

Take a Tax Break

Although this will be determined by your adjusted gross annual income, you might be able to take advantage of a number of federal tax breaks such as the Lifetime Learning Credit, or the American Opportunity Tax Credit for the years you are paying for your child’s college education.

-

Repayment Plans Can Be Flexible

They are available, and they do exist! It is possible to reduce the costs once your child has graduated and the requirements to start repaying any loans kicks-in. In certain circumstances, of you set-up a direct debit, there is often a discount available for that particular type of payment method. Federal loans for students are often a little more flexible as opposed to loans for private education students.

-

Get More Control With A Custodial Account

If you gift an asset via the Uniform Gifts to Minors Act (UGMA), or you move these assets via the Uniform Transfers to Minors Acts (UTMA), this increases the number of investments options that you will then have. There is, however, a small caveat with this option. UTMA and UGMA accounts can impact more on financial aid decisions due to the fact they are viewed as an asset belonging to the child and not to the parents. There are fewer tax benefits as opposed to a 529 or Coverdell savings arrangement too. The other really important point to note is that regardless of whether your child goes to college, the money will become theirs at either the age of 18 or 21.

Even with these increased costs of education that are present in today’s world, it is still the most beneficial, and cost-effective way to ensure that your loved ones get the best start possible. The earning potential of a graduate with a Bachelors Degree is much, much higher than of someone without this qualification. This makes saving for a college education still a top priority and concern for most parents.